Healthcare Quarterly

Publicly Financed Healthcare and Income Inequality in Canada

Lisa Corscadden, Sara Allin, Michael Wolfson and Michel Grignon

Abstract

Income inequality is currently the focus of considerable public and policy attention. Public services such as healthcare and education play a role in reducing income inequality in the population. This study looks at how healthcare affects the distribution of income across five income groups. Specifically, it estimates the tax contributions and the value of benefits received from physician services, drugs and hospital services over a person's lifetime. We found that benefits received from publicly funded healthcare in Canada reduce the income gap between the highest- and lowest-income groups by 16%. This analysis provides a starting point for future research to explore the distributional effects of different options for financing healthcare.

In addition to being a valuable public service, publicly financed healthcare plays another role that is often overlooked: it redistributes income from higher- to lower-income groups. In a recent Canadian Institute for Health Information (CIHI) study, we estimated the value of benefits received from publicly financed drugs, hospitals and physician services over a person's lifetime and added it to the individual's lifetime income (CIHI 2013). Then we looked at how this additional "income source" affected income inequality.

Other studies have shown that in countries with tax-financed health systems such as Canada, if the dollar value of health benefits received is added to people's income, income inequality is reduced (Organisation for Economic Co-operation and Development [OECD] 2008; Verbist et al. 2012). This effect has also been demonstrated in two Canadian provinces (McGrail 2007; Mustard et al. 1998). An important limitation with this literature is that healthcare taxes and benefits are measured at a single point in time.

The current study addresses this limitation by taking a life course approach, similar to studies done in Australia and the United Kingdom (Harding et al. 2002; Propper 1995). A life course approach accounts for two important factors: that people tend to earn more and pay more in taxes when they are middle-aged and to use more healthcare services when they are older; and those in higher-income groups tend to live longer than those in lower-income groups and therefore benefit from publicly funded healthcare services longer.

Methods

The analysis proceeded in four steps. First, we estimated healthcare costs by age and income group using the most recently available administrative and survey data on the three largest components of health spending, hospitals, physicians and publicly funded drugs. Second, we estimated payments to healthcare – the income and consumption taxes paid to fund healthcare (assuming all health costs are financed by household taxes) by each age and income group using the Statistics Canada Social Policy Simulation Database and Model (SPSD/M). Third, we estimated the costs and payments over the lifetime for each income and sex group using a micro-simulation tool called Modgen (model generator) by projecting health costs and tax patterns over an adult life course, under current patterns of mortality by age, sex and income (Statistics Canada 2013). Finally, we estimated income inequality as the ratio of average income in the highest-income group compared with that in the lowest-income group both before and after adding the dollar value of the health benefits received and subtracting tax payments.

Results

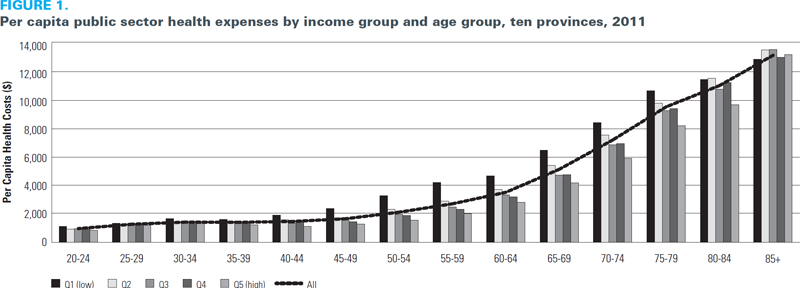

As expected, we observed that health costs increase with age for all income groups and decrease with income. Within each age group, there was an income gradient whereby the lower-income groups on average used more health services, and thereby incurred more health costs, than those with higher income (Figure 1). However, the income gradient taken over the life course was smaller than the one observed cross-sectionally (all ages taken together), in part because, on average, people with the highest income live longer than those with the lowest income. On average, the lifetime healthcare costs were estimated to be $237,500 per person in the lowest-income group compared with $206,000 in the highest-income group; this represents a difference of only 15%, compared to a difference of 60% when we considered the health costs incurred at a single point in time.

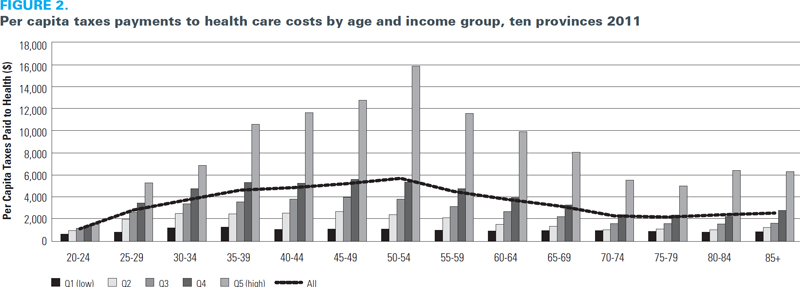

Also as we would expect, we observed significant variations in tax payments by age, with the highest contributions evidenced in the middle years and lowest in the younger and older ages (Figure 2). Given the structure of the tax system, the highest-income group paid considerably more in taxes to fund healthcare than the four lower-income groups, and alone the tax payments of the highest-income group accounted for almost half of the total taxes available for healthcare.

Given that the highest-income group contributed more to fund healthcare but received proportionally less in health benefits than lower-income individuals, we would expect that healthcare has the effect of reducing income inequality in the population. As shown in Table 1, people in the highest-income group earned an average of $115,000 annually over their lifetime, of which they paid about 7.5% (or $8,650) toward publicly financed health costs. People in the lowest-income group, while paying a lower amount toward taxes ($1,020), still paid 6% of their $17,500 average yearly income toward health costs. Average annual healthcare costs represent a much larger proportion of the income of the lowest-income group, at 24% compared with only 43% of the highest-income group's average income after taxes.

| TABLE 1. Annualized lifetime health care costs and payments in relation to income | ||||||

| Annualized Lifetime | Q1 (low) | Q2 | Q3 | Q4 | Q5 (high) | Ratio Q5/Q1 |

| Average income ($) | 17,500 | 31,400 | 43,900 | 60,100 | 114,900 | 6.6 |

| Tax payments to healthcare ($) | 1,020 | 1,910 | 2,780 | 3,960 | 8,650 | |

| Tax payments to healthcare as a percent of income (%) | 5.80% | 6.10% | 6.30% | 6.60% | 7.50% | |

| Healthcare costs ($) | 4,220 | 3,820 | 3,650 | 3,650 | 3,350 | |

| Healthcare costs as a percent of income (%) | 24.10% | 12.20% | 8.30% | 6.10% | 2.90% | |

| Net gain or loss (healthcare costs-taxes) ($) | 3,200 | 1,910 | 870 | -310 | -5,300 | |

| Net gain or loss as a percent of income (%) | 18.30% | 6.10% | 2.00% | -0.50% | -4.60% | |

| Average disposable income* ($) | 17,370 | 28,400 | 37,830 | 49,740 | 89,220 | 5.1 |

| Average disposable income* + healthcare cost ($)* | 21,590 | 32,220 | 41,480 | 53,390 | 92,570 | 4.3 |

| *Disposable income represents the total household income plus transfers and capital gains minus income taxes. It is adjusted for household size and assigned to each individual in the household. | ||||||

Income inequality, as measured by the gap in income between the highest- and lowest-income groups, was lower after accounting for tax payments and benefits received from healthcare. Specifically, the highest-income group had average annual income that was 6.6 times that of the lowest-income group; this was reduced to 5.1 times after accounting for total taxes paid, and further reduced to 4.3 times after adding the dollar value of health costs as a benefit in kind (in a similar way one might add the value of a childcare benefit, for example). In other words, incorporating the value of services received through publicly financed health evened out the distribution of income across income groups.

Discussion and Conclusions

This study represents an important step in estimating the distributional effects of publicly financed healthcare from a life course perspective. Healthcare in Canada is mostly financed through taxation, based on individuals' ability to pay, and is delivered on the basis of need. This study shows that, as would be expected, the tax system in Canada redistributes income from the higher- to lower-income groups (reducing the gap in lifetime income from 6.6 to 5.1, or 23%). This study also estimates that adding the value of healthcare services received to average income, thus treating it as an in-kind benefit, further reduces the gap in lifetime disposable income from 5.1 to 4.3 or by another 16%.

Future analyses could look at the effects of potential policy changes to health financing, including the distributional effects of different mixes of provincial and federal funding or changes to the mix of revenue sources from income and commodity taxes. Other key improvements to the model would be to incorporate changes in people's income level and changes to their level of health over their lifetime in order to better separate out income transfers between healthy and sick groups. Further research could also explore the different types of healthcare costs separately to better understand their respective impacts on the income distribution. With these improvements, models such as this would more readily enable researchers to test the distributional consequences of changes to healthcare use or financing. As publicly financed healthcare does play a role in redistributing income, changes to healthcare financing policy can also be considered for their distributional effects in a more systematic way, similar to the analyses undertaken for tax policy options.

About the Author(s)

Lisa Corscadden, MSc, is a senior researcher with the Bureau of Health Information, New South Wales, Australia, and was a program consultant with Canadian Institute for Health Information (CIHI) at the time of this writing. She can be contacted by e-mail at Lisa.Corscadden@bhi.nsw.gov.au.

Sara Allin, PhD, is a senior researcher with CIHI and an assistant professor, status only, with the School of Public Policy and Governance, and the Institute for Health Policy, Management and Evaluations at the University of Toronto, in Toronto, Ontario.

Michael Wolfson, PhD, is Canada research chair in population health modelling/populomics at the University of Ottawa, in Ottawa, Ontario.

Michel Grignon, PhD, is the director of the Centre for Health Economics and Policy Analysis, and an associate professor in the Department of Health, Aging and Society and the Department of Economics at McMaster University, in Hamilton, Ontario.

References

Canadian Institute for Health Information. 2013. Lifetime Distributional Effects of Publicly Financed Health Care in Canada. Ottawa, ON: Author.

Harding, A., R. Percival, D. Schofield and A. Walker. 2002. "The Lifetime Distributional Impact of Government Health Outlays." Australian Economic Review 35(4): 363–79.

McGrail, K. 2007. "Medicare Financing and Redistribution in British Columbia in 1992 and 2002." Healthcare Policy 2(4): 123–37.

Mustard, C.A., M. Barer, R.G. Evan, J. Horne, T. Mayer and S. Derksen. 1998, October. Paying Taxes and Using Health Care Services: The Distributional Consequences of Tax Financed Universal Health Insurance in a Canadian Province. Presented at the CSLS Conference on the State of Living Standards and the Quality of Life in Canada, Ottawa, ON.

Organisation for Economic Co-operation and Development. 2008. Growing Unequal? Income Distribution and Poverty in OECD Countries. Paris, France: OECD Publishing.

Propper, C. 1995. "For Richer, for Poorer, in Sickness and in Health: The Lifetime Distribution of NHS Health Care." In J. Falkingham and J. Hills, eds., The Dynamic of Welfare. London: Harvester Wheatsheaf.

Statistics Canada. 2013. MODGEN Developer's Guide. Ottawa, ON: Author. Retrieved March 18, 2014. <http://www.statcan.gc.ca/microsimulation/modgen/doc/devguide/dev-guide-eng.htm>.

Verbist, G., M. Forster and M. Vaalavuo. 2012. The Impact of Publicly Provided Services on the Distribution of Resources (OECD Social, Employment and Migration Working Paper, No. 130). Paris, France: OECD Publishing. DOI: 10.1787/5k9h363c5szq-en.

Comments

Be the first to comment on this!

Personal Subscriber? Sign In

Note: Please enter a display name. Your email address will not be publically displayed