ElectronicHealthcare

The HIT Report from KLAS: The Filmless Revolution; Focus: Picture Archive and Communication Systems (PACS)

Abstract

This extract, from a recent PACS study, offers unique insight into the performance, underlying technology, product depth and breath and "real world" issues facing eight of the leading PACS vendors and their clients as rated at more than 130 of their client sites and from over 300 CIOs, department directors and vendor executives. The full report contains over 250 pages of rankings, commentaries and analysis and was published June 2001 by KLAS.

The filmless revolution

The driving force behind this report reflects the heightened interest in PACS systems in general and their contributions to the benefits associated with an electronic medical record. Ten healthcare provider organizations, ranging from a 150-bed Acute-Care Hospital to a 7-hospital IDN, sponsored the research. Most of the data in the report focuses on the use of PACS in the radiology department, as few sites are using PACS systems in other departments as can be seen in the departmental use of PACS graph.

PACS networks installed by Agfa, Canon Medical Systems, DR Systems, GE Medical Systems, Kodak Health Imaging, Marconi Medical Systems, Philips and Siemens Medical Solutions were surveyed. With few exceptions, buyers narrow down their choice to 2-3 of these vendors. Several PACS vendors were not included (conscious choice) because they were either a newcomer, or because they do not offer enough of a full PACS solution to be included at this time. All 8 vendors are considered viable solutions in their ability to automate and archive diagnostic images in order to improve clinician access and patient care.

Putting client comments into perspective

The participating vendors supplied KLAS with their customer lists, which contributed to the majority of clients surveyed. Clients surveyed in the study varied widely in size, ranging from 50-2000 beds, however, forty-six percent (46%) of those surveyed were over 400 beds.

The customers represented a broad cross-section of PACS users, ranging from 10% to 95% filmless, with large-scale users making up the majority of respondents. Each of the customers were asked to numerically rate their vendor on 28 aspects of performance, as well as answer 12 questions relating to customer satisfaction.

14 Primary Indicators of Performance

- Lived Up to Expectations

- Vendor Is Improving

- Proactive Service

- Quality: Money's Worth

- Commitment to Technology

- Executives Interested in You

- Good Contracting Experience

- Product Works as Expected

- Quality of Training

- Quality of Implementation

- Quality of Telephone Support

- Quality of Interface Services

- 3rd Party Product Works w/Vendor Products

- Helps Your Job Performance

14 Detailed Performance Indicators

- Worth the Effort

- Real Problem Resolution

- Good Job Selling

- Product Quality Rating

- Implementation on Time

- Implementation within Budget

- Quality of Implementation Staff

- Quality of Documentation

- Quality of Releases & Updates

- S/W Errors Corrected Quickly

- Interfaces Met Deadlines

- Quality of Custom Work

- Hardware Vendor Satisfaction

- Response Times

12 Key Indicators of Satisfaction Implemented in the Last 3 Years

- Core Part of IS Plan

- Would you buy it again?

- Avoids Nickel and Diming

- Keeps All Promises

- A Fair Contract

- Contract is Complete

- Contract Administered Fairly

- Timely Enhancement Releases

- Support Costs as Expected

- Ranked Client's Best Vendor

- Ranked Client's Second Best Vendor

While Philips enjoys the top overall rating each vendor has strong points reflected in the comparison, and 7 of the 8 vendors were rated at least first or second in some category.

Select key business indicators

The following graph represents the survey results of select key business indicators measured.

Unique to this survey

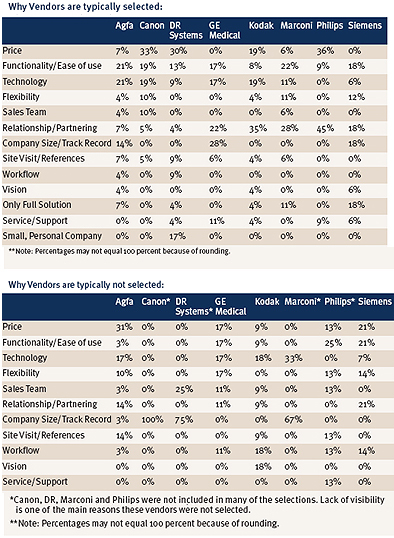

In addition to PACS clients, the PACS vendors themselves were interviewed and interview questions involved their self perception regarding: why they win, where they can improve and who they regard as their competitor. The following two graphs combine both vendor and client comments regarding why vendors are "typically selected" or "not selected."

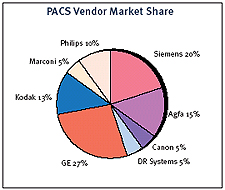

Survey participants market share

Trying to assess a vendor's market share is always difficult and in the case of PACS it would clearly depend on how you wanted to count partial implementations, mini-PACS, teleradiology, etc. As qualified, as it may seem, it is of interest to understand, as best as possible a vendor's market share. The following pie chart represents the market share for the 8 vendors that qualified for assessment in this specific study.

Offer to Canadian Healthcare Facilities

Many Canadian Healthcare facilities and organizations use vendors who supply solutions unique to Canada. KLAS - the organization rating IT vendors in this and subsequent issues of ElectronicHealthcare - is willing to gather confidential and candid data from Canadian healthcare executives and provide access to the results to the all data contributors. The vehicle that will be used is the web based KLAS vendor evaluation form found at www.healthcomputing.com under "rate your vendor" button. If you are interested in participating please contact Mr. Ralph Reyes Jr., Senior Vice President, KLAS Enterprises LLC. Telephone: 866-268-9438. Email: ralph@ healthcomputing.com.

If you have comments, suggestions or questions about this vendor-rating feature please send an email to editors@longwoods.com.

ADDENDUM

Due to its beginning focus on select aspects of PACS (mini-PACS), and later entry into the enterprise PACS market, A.L.I. Technologies Inc. (ALI) was not originally included as part of the original June 2001 KLAS PACS study. Furthermore due to its relative "newness" in the market and focus on select aspects of PACS, Stentor's iSite™ was not originally included as part of the original June 2001 KLAS PACS study.

Upon issuance of the report, however, both ALI and Stentor asked that a similar assessment be made of the their products and included as an addendum to the June 2001 KLAS PACS study. An addendum representing research performed in September 2001 in response to the ALI and Stentor requests is available at www.ElectronicHealthcare.net. The reviews represent assessments from 10 provider organizations for ALI and 18 provider organizations for Stentor.

About the Author(s)

ABOUT KLAS

Who We Are

KLAS, founded in 1996, is the only research and consulting firm specializing in monitoring and reporting the performance of Healthcare Information Technology (HIT) vendors . Our staff and advisory board average 25 years of healthcare information technology experience.

How We Serve the Healthcare Industry

KLAS, in concert with thousands of Healthcare Executives, CIOs, Directors, Managers and Clinicians has created a dynamic database of information on

the performance of HIT vendors. The KLAS database represents the opinions of healthcare executives, managers and clinicians from over 3000 healthcare

facilities on 180+ vendors and 300+ different products. The information is continually refreshed with new performance evaluations and interviews

daily. The KLAS database is dynamically and effectively used by:

- Healthcare organizations to align expectations with a vendor's actual performance, to assist in strategic planning and to validate decision processes.

- Vendors to monitor their performance in comparison with competitors.

- Consultants for current performance information on a specific company or product.

- Healthcare investment firms to evaluate publicly traded HIT company trends.

Contact KLAS at www.healthcomputing.com or 866-268-9438.

Comments

Be the first to comment on this!

Personal Subscriber? Sign In

Note: Please enter a display name. Your email address will not be publically displayed